Power projects in Tanzania represent a key driver of the nation’s energy landscape. As the demand for reliable electricity continues to rise, understanding the intricacies of these projects becomes essential for both investors and stakeholders alike. In this month’s legal update, we explore Tanzania’s power sector including its project financing structure, financing sources, equity dynamics, and the status of Government guarantees.

Tanzania Power Sector Framework

The Ministry of Energy (the Ministry) oversees Tanzania’s power sector, responsible for creating and assessing Government policies related to power and gas. The Ministry also takes steps to organise the power sector and negotiates agreements on behalf of the Government of Tanzania (GoT). The primary legislation relevant to electricity is the Electricity Act 2008 and its accompanying regulations.

Tanzania Electric Supply Company (TANESCO), the state-owned utility, is responsible for generating, transmitting, distributing, and selling electricity throughout the country. TANESCO owns and operates transmission and distribution systems under GoT ownership, and its activities are overseen by the Ministry. It is the key offtaker to independent power projects such as Songas. By utilising the country’s own natural gas resources, Songas offers a form of energy which adds to the country’s energy mix. Songas and certain other private independent power producers have a single client in TANESCO.

The Energy and Water Utility Regulatory Authority (EWURA) is tasked with regulating the power sector. Established in 2006 through the Electricity and Water Utilities Regulatory Authority Act of 2001, EWURA oversees power, water, and certain aspects of the petroleum and natural gas sectors. It issues licenses for approved electricity activities under the Electricity Act of 2008 and approves and enforces tariffs and fees for licensees. Additionally, EWURA reviews the terms of electricity supply agreements, including Power Purchase Agreements (PPAs), working in consultation with the Minister of Energy.

The Rural Energy Agency (REA) focuses on improving energy services in rural areas by implementing solutions such as mini-grids and off-grid solutions. It funds rural energy projects through the Rural Energy Fund, providing grants to cover capital expenses. The legislation underpinning rural energy is the Rural Energy Act 2005.

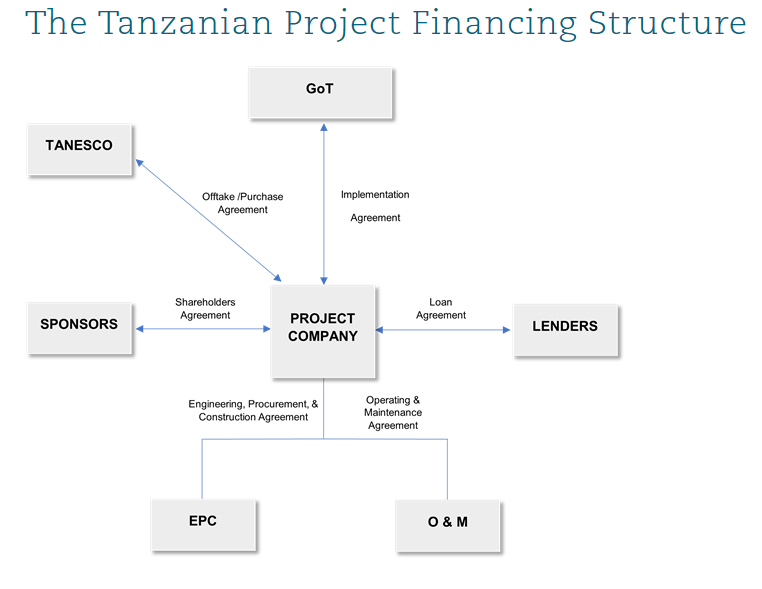

The structure of the various parties to a project finance transaction involves the project company, sponsors/developers, shareholders, lenders, TANESCO and GoT.

The project company (typically owned by the sponsors) takes the form of a special purpose vehicle, specifically created to undertake a single project. It will establish agreements with the Government, suppliers, contractors, operators, and with the lenders and financing parties.

Financing the Power Project

Power projects in Tanzania typically secure funding through a combination of debt and equity, both playing essential roles in the financing structure. The ratio of debt to equity, often referred to as the “gearing” or “leverage ratio,” is determined by factors such as the project’s available cash flow and perceived risks. It is traditionally 70 (debt) : 30 (equity).

The sources of debt funding are diverse and cater to different project requirements. Various lenders have distinct objectives, influencing their participation and pricing strategies. Significant funding, known as “senior debt,” is supplied by financial institutions and comes with longer repayment periods, often spanning a decade or more. On the other hand, subordinated debt, sometimes called “mezzanine debt,” is provided by institutions that accept a lower priority in terms of cash flow and contractual rights, making it a comparatively higher-cost option.

While Development Finance Institutions (DFIs) like the African Development Bank, International Finance Corporation, and British International Investment (formerly CDC) are traditional lenders to Tanzanian power projects. Other entities such as export credit agencies (ECAs) and commercial banks can also participate as lenders in power projects.

Equity sources are equally crucial, often requiring project sponsors to contribute in alignment with agreed gearing levels. Sponsors and developers hold significant equity stakes, while additional funding might come from private equity funds, venture capital, and impact investors.

It should be noted, however, that a typical Tanzanian project financing revolves around limited or non-recourse transaction structures. This means that if the project company encounters financial challenges, the lenders may decide to ‘step into the shoes’ of the project company through step in rights contained in a Lenders Direct Agreement.

Are Government guarantees available? What options are there for bolstering the creditworthiness of the offtaker?

African power projects will often require a Government guarantee of the offtakers payment obligations under the PPA.

However, at the time of writing, Government guarantees for power projects are generally not available in Tanzania. Private parties are encouraged to finance and structure projects on their commercial merits alone.

Given the lack of availability of Government guarantees, other liquidity options must be considered including:

- Escrow Accounts: Escrow accounts with a certain amount of months of PPA repayment (and debt service) are an option.

- Letters of Credit (LC): LCs from Banks with a certain amount of months of PPA repayment (and debt service) are an additional option. LCs are a relative expensive choice for the parties.

- Government letters of support: Although not as strong as a Government guarantee, Government letters of support may form part of the liquidity support package.

- Political risk insurance: Entities such as the Multilateral Investment Guarantee Agency (MIGA) or Africa Trade Insurance will often offer insurance options to the project company.

- DFI partial risk guarantees: DFIs such as African Development Bank and Agence française de développement offer partial risk guarantees which are part of the liquidity mitigation.

Source : Clyde & Co